ブログ

Why Japan Is Becoming a Strategic Choice for Asian Startups ── TSE Asia Startup Hub × TMI Singapore Office Dialogue ── APAC Frontier Dialogue Vol. 1

2026.04.27

SHARE![]()

![]()

![]()

INTRODUCTION

In this blog series, we explore a broad range of topics, including the practice areas supported by Japanese law-qualified lawyers in overseas offices and recent business trends, from a perspective that differs slightly from corporate legal practice in Japan.

The Singapore office of TMI Associates hosts a large number of Japan-qualified lawyers who are engaged in a diverse range of matters across Southeast Asia. While supporting Japanese companies in their overseas expansion, as well as handling various cross-border corporate matters such as M&A and financing transactions, one area that has gained increasing prominence in recent years is the support of Asian startups entering the Japanese market and pursuing IPOs on the Tokyo Stock Exchange ("TSE").

In this first part of the series, we present a discussion featuring Tatsuaki Sato of the TMI Singapore office, who is closely involved in supporting Asian companies entering Japan with a view to future listings on the TSE. The session highlights insights shared in conversation with a member of the New Listings Department of the TSE, who is leading the “TSE Asia Startup Hub” initiative.

Dialogue Participant Profiles

| Junichiro Goto, New Listings Department, Tokyo Stock Exchange With over 10 years of experience at the Tokyo Stock Exchange supporting overseas companies and startups in listing on the TSE, he is currently responsible for the “TSE Asia Startup Hub” initiative. |

| Tatsuaki Sato, Attorney at Law admitted in Japan, MBA(TMI Associates, Singapore Office) Having joined TMI Associates in 2014, Sato was seconded to the Listed Company Compliance Department and the Listing Examination Department of Japan Exchange Regulation between 2016 and 2018, where he worked on listing-related reviews and the development of the Principles for Preventing Corporate Scandals. He completed an MBA at the National University of Singapore Business School in 2022 and is currently based in the Singapore office. His practice focuses on startup-related matters in Southeast Asia, cross-border M&A, and corporate inversion (Japan flip) transactions. He is a co-author of Legal Practice for Startups (Shojihomu), among other publications. |

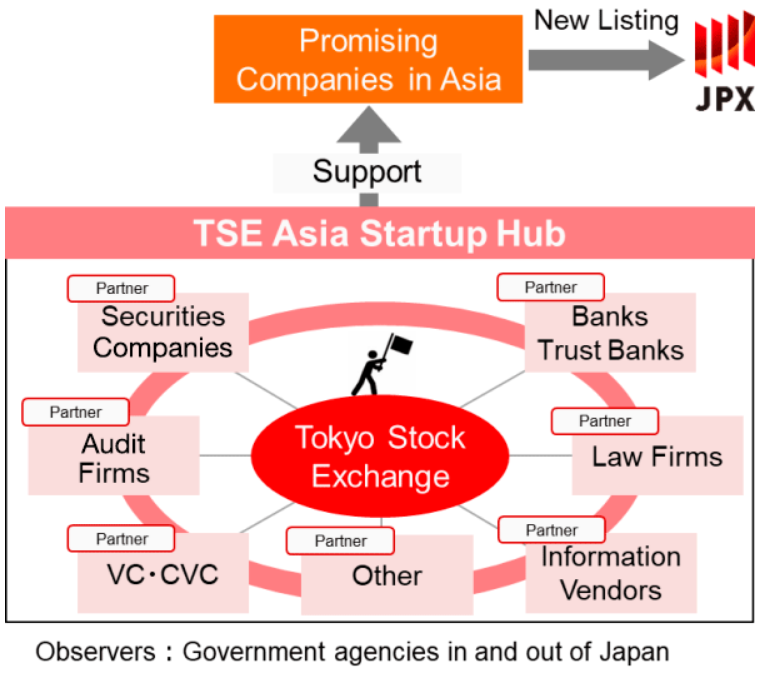

In March 2024, the TSE launched the “TSE Asia Startup Hub”. As of 2026, 20 startups from seven countries and regions, including Singapore, Taiwan, and South Korea, have been selected for the program. Supported by a broad network of partners such as securities firms, audit firms, law firms, venture capital firms, and banks, this initiative represents an unprecedented effort for a Japanese stock exchange.

(Source: Japan Exchange Group website)

As noted in the materials presented at the 4th Meeting of the Japan Growth Strategy Council under the Japan Growth Strategy Headquarters (established within the Cabinet), dated 22 April, 2026, entitled "Direction for Addressing Cross-Sectoral Challenges" — in which the Japanese government explicitly stated its intention to "work in collaboration with the Tokyo Stock Exchange and other entities to support promising overseas startups from their entry into the Japanese market through to their listing on the TSE, thereby strengthening the startup ecosystems in Japan and abroad" — the listing of foreign companies on the TSE is creating new momentum in the capital markets.

We present a discussion between Tatsuaki Sato, who previously worked on secondment at Japan Exchange Group and is currently engaged in startup and IPO support matters at the TMI Singapore office, and Junichiro Goto of the New Listings Department of the TSE, who is involved in the TSE Asia Startup Hub initiative. In this discussion, they share insights on the objectives of the program and its interface with corporate legal practice.

What Is the TSE Asia Startup Hub?──An Ecosystem Beyond Listing Promotion

── It has been nearly two years since the launch of the “TSE Asia Startup Hub” in March 2024. To begin, could you briefly walk us through the background to its establishment and its current status?

Goto

The TSE Asia Startup Hub is an ecosystem designed to support, from a medium- to long-term perspective, IPOs on the TSE by providing tailored support to high-growth Asian companies in line with their specific needs, including business development and fundraising in Japan as well as IPO readiness. It represents an unprecedented initiative for the TSE, bringing together a broad range of professional institutions such as securities firms, audit firms, banks, and venture capital firms to collectively support participating companies in their expansion into the Japanese market.

While the New Listings Department of the TSE has long engaged in efforts to promote listings by overseas companies, we recognised that, for high-growth Asian startups to establish a meaningful presence in the Japanese market, support is required from a much earlier stage than the listing examination process. In light of this, the TSE Asia Startup Hub was established with the aim of creating an ecosystem that facilitates collaboration by providing early-stage touchpoints. This enables participating foreign companies to work closely with professional advisors from the point of market entry into Japan, including the establishment of local operations and the development of partnerships with Japanese companies, through to their eventual listing journey.

The inclusion of law firms as partners of the TSE Asia Startup Hub reflects our view that, for foreign companies entering Japan, legal and compliance needs arise at a very early stage. The establishment of a Japanese entity, preparation of contracts with Japanese counterparties, drafting of terms of use, and compliance with various regulatory requirements are all essential steps in launching a business. In addition, the involvement of professionals is indispensable in building a corporate governance framework with a view to a future IPO. Furthermore, when a foreign company files a securities registration statement, it is standard practice for Japanese counsel to act as its representative and handle the related filing procedures. From this perspective, the participation of full-service corporate law firms, including TMI Associates, as partners provides a significant source of assurance for the companies supported under the program.

Sato

Thank you for walking me through that. Our decision to partner with the TSE Asia Startup Hub stems from our strong resonance with the views you have outlined.

For Asian companies entering Japan, there are a wide range of legal and compliance challenges and latent needs that arise from the initial stage, such as the establishment of a Japanese entity, through to the stage where an IPO is seriously contemplated, and even beyond listing. For such companies, this TSE initiative, which increases touchpoints with various professional partners in Japan, is highly meaningful. Matters such as contract negotiations tailored to the specific characteristics of each business, protection of intellectual property, employment laws and regulations, personal data protection, and compliance with foreign exchange regulations are all critical. Whether these are properly addressed from an early stage has a significant impact on the level of trust in a company’s operations in Japan, and in turn contributes positively to business growth and IPO readiness.

── We understand that the TSE Asia Startup Hub selects as target companies those aiming to list on the TSE within the next three to five years. To begin, we would like to ask you to explain the background to this approach.

Goto

Under this initiative, the ultimate objective is to create an environment in which high-growth Asian companies can more readily list on the TSE. It does not require participating companies to achieve a listing on the TSE within a short timeframe. It is assumed that the business environment surrounding startups and their growth strategies will evolve over time, and decisions regarding the timing of listing should be made based on what is most appropriate for each company’s business strategy. Accordingly, it is not the intention of the TSE to fix, from the outset, the timing of listing or to impose constraints on companies’ future business activities.

The TSE Asia Startup Hub places primary emphasis on supporting companies in developing their businesses in Japan and fostering collaboration with Japanese companies, thereby deepening their engagement with the Japanese market. Through these efforts, we believe that enabling participating companies to build relationships with Japanese investors and corporates will, in itself, contribute to the revitalisation of the Japanese economy. In practice, since the launch of the program, some companies have successfully entered into business partnerships with Japanese companies, while others have commenced service offerings in Japan. Although progress has been gradual, we are beginning to see tangible results from these activities.

Sato

I believe that TSE’s position of not requiring a near-term listing is a highly meaningful and important choice in building trust with participating companies. The path to fundraising and IPO for startups is inherently fluid, and the decision to list on TSE is typically one that develops over several years.

At the same time, we believe that TSE’s sustained commitment to working closely with Asian companies, encouraging them first to build a track record in Japan, serves as a key factor in strengthening trust. This, in turn, may ultimately become a decisive factor when Asian companies come to make their listing decisions in the future.

The Initiative’s Current Position ──Singapore as a Base and TSE’s Strengths in Asia

── Since the launch of the TSE Asia Startup Hub, we would like to ask you to outline the current state of its activities.

Goto

In September 2024, we announced the first cohort of 14 selected companies, and in September 2025, we announced a new group of 20 companies, including newly selected participants. The program has also expanded its geographic reach, now covering Singapore, Taiwan, South Korea, Malaysia, Indonesia, Vietnam, and the Philippines. The sectors represented are diverse, including AI, healthcare, fintech, drones, and SaaS. Participating companies have shared that their involvement in this program has helped advance both their business expansion in Japan and their IPO preparations. Overall, we are seeing the ecosystem steadily gain traction and become more firmly established.

With respect to our initiatives in Singapore, TSE conducts annual IPO seminars and provides opportunities for business matching between local startups and Japanese listed companies. From TSE’s perspective, Singapore is positioned as one of the key hubs for the activities of the TSE Asia Startup Hub.

Singapore hosts a strong concentration of leading Southeast Asian startups, as well as a deep pool of financial and investment players, including venture capital firms and institutional investors, alongside regional bases of Japanese companies. This creates an optimal environment for the TSE Asia Startup Hub ecosystem to function effectively. In addition, many of the Hub’s partners have a presence in Singapore, making it easier to establish coordinated local support and collaboration frameworks. The fact that a significant number of participating companies have Singapore incorporated entities also reflects the strength of this well-developed ecosystem.

Sato

Singapore is often chosen as a regional business hub in Southeast Asia. While the center of marketing or operations may be located in countries such as Vietnam or Indonesia, it is not uncommon for the core entity to be incorporated in Singapore. We believe that this longstanding trend is one of the reasons why many of the companies supported under the TSE Asia Startup Hub have Singapore incorporated entities.

From my perspective, having studied at the business school of National University of Singapore and continuing to engage closely with startups, I sense that their interest in Japan is steadily increasing. What is changing here is the nature of that interest. The earlier perception that “Japan is a difficult market for business expansion or partnerships” is gradually fading. Instead, more startup stakeholders are beginning to view Japan as a target market for growth and as part of a forward-looking strategy, for example by enhancing credibility through partnerships with established Japanese companies and accelerating global expansion through a listing on TSE.

We believe that this reflects both changes in the external environment, such as the gradual easing of language barriers due to technological advances, and a shift in mindset among Japanese listed companies, which are increasingly seeking to engage with overseas companies and markets.

── From the perspective of Asian startups, what are the specific advantages of choosing TSE as a listing venue?

Goto

From the perspective of the overall market, TSE is one of the largest exchanges in Asia in terms of market capitalisation and boasts among the highest trading volumes and numbers of listed companies globally. The Nikkei 225 has also reached record highs in recent years, and the market as a whole has remained active, continuing to attract strong interest from overseas institutional investors. This dynamic market environment is a significant attraction for Asian startups, particularly in terms of post-listing fundraising capacity and share liquidity.

TSE currently operates three core market segments, namely Prime, Standard, and Growth. Among these, the Growth market is characterised by participation from both retail and institutional investors. In addition to facilitating smoother and more diversified fundraising through listing, companies can also expect enhanced visibility and brand recognition as a TSE-listed company, strengthened credibility with business partners and financial institutions, and improved ability to attract high-quality talent.

In comparison with the US markets, TSE’s strengths lie in its cultural and geographic proximity to Asia, as well as its “All Japan” ecosystem. For startups with market capitalisations in the range of several tens to hundreds of billions of yen, the US markets can present a high barrier to entry, and maintaining share price performance post-listing may not be straightforward. TSE, by contrast, is a market that can provide such companies with access to a broad investor base and liquidity, and we believe its visibility across Asia is continuing to grow. We also continue to engage in listing promotion activities to ensure that more companies understand the advantages of the TSE market.

Sato

Building on the points you have raised, we believe that the effect of a TSE listing as a form of “credibility endorsement” in the Japanese market is highly significant. From my personal experience through an Asian MBA program, one impression that has remained particularly strong is that, among business professionals across Asia, the level of interest in and regard for the “Japan” brand and the TSE market is still far higher than many in Japan might expect.

Being listed on TSE serves as a signal of financial transparency and business continuity to counterparties and financial institutions. This is not limited to Japan but extends across Asia and globally. For startups seeking to scale their business internationally, such a listing enhances credibility and adds value, and many Asian companies view this as a key advantage with direct relevance to their future global expansion.

Cultivating a “Japan Flavor”

── We understand that the TSE Asia Startup Hub is not focused solely on supporting companies aiming to list on TSE, but rather on supporting companies that possess a “Japan flavor” or a “Connection with Japan.” We would like to ask you to elaborate further on this point.

Goto

In selecting companies for support under the TSE Asia Startup Hub, the key consideration is not simply whether a company has an intention for IPO on TSE, but whether it has a genuine commitment to developing its business in Japan. A proactive approach to business expansion in Japan is what fosters trust with investors and counterparties and, in turn, helps to steadily build the foundation for a future listing, secure post-listing liquidity, and support share price stability.

For the TSE Asia Startup Hub, the objective is to encourage overseas startups to view Japan as a platform for new business development, fundraising, and commercial opportunities. By achieving growth in Japan, these companies become more readily accepted by Japanese investors, and a future listing further enhances their credibility both domestically and internationally, enabling their businesses to expand across Asia and globally. The aim is to create this virtuous cycle.

Our message is that, even for companies that currently have limited ties to Japan, we will provide support through the TSE Asia Startup Hub if they are willing to position Japan as a key market in their management strategy and are committed to advancing business operations in Japan, including pursuing capital and business partnerships with Japanese companies.

Sato

We believe that a business with a “Japan flavor” is cultivated through the accumulation of practical experience over time. While this is not unique to Japan, expansion into any foreign market requires companies to proceed in parallel with both an understanding of local business practices and compliance with jurisdiction-specific regulatory requirements.

In a B to C business model, it is of course essential to gain a detailed understanding of the characteristics of Japanese users. However, even in B to B businesses, matters such as preparing and reviewing contracts in line with Japanese market practice, complying with personal data protection and foreign exchange regulations, and filing for trademarks and patents cannot be deferred. Expanding a business while postponing these steps may lead to unforeseen costs and risks emerging at a later stage. From the perspective of someone who has studied both law and business across multiple jurisdictions, legal frameworks form the foundation of business, while commercial practices often inform the underlying basis for regulation. In that sense, local business practices and regulatory frameworks are mutually interconnected and operate in a continuous, reinforcing cycle.

From a different perspective, in relation to IPOs, the type of compliance measures and governance structures described above are not always practical for startups to establish at significant cost from an early stage. In many cases, it may be more common for companies to gradually strengthen these frameworks once an IPO becomes a realistic prospect.

However, by being mindful of these considerations from the early stages of entering the Japanese market, and by identifying and addressing material legal risks at an early stage while developing the business, companies can anticipate and mitigate critical issues before they arise, ultimately resulting in a significant reduction in time and cost.

By pursuing such a phased strengthening of compliance in preparation for an IPO, companies will be better positioned to respond smoothly to audits by accounting firms, reviews by securities firms, and examinations by the exchange. From this practical perspective as well, we believe that the TSE Asia Startup Hub’s efforts to build an ecosystem are well founded from both an offensive and defensive standpoint.

Legal Issues in a Tokyo Stock Exchange Listing ── CI or JDR: The Importance of Early Consultation

── When overseas companies reach the stage of pursuing a listing on TSE, what legal issues typically arise?

Sato

When a foreign company considers listing on TSE, there are broadly two approaches. One is through Japanese Depositary Receipts ("JDR"), whereby the company remains a foreign entity and lists in Japan by issuing securities backed by its foreign shares. This approach is attractive for foreign companies as it allows them to pursue a TSE listing without changing their existing corporate structure. As JDRs are trust beneficiary interests, support from a trust bank is particularly important, which represents a key difference from a typical domestic listing in Japan.

The other approach is Corporate Inversion ("CI"), also called Japan flip, whereby the group is restructured with a Japanese entity as the holding company, and the listing is pursued on a Japan-based corporate structure. As this approach is closely intertwined with existing equity rounds and the timing of post reorganisation audits, it typically requires planning over a multi-year horizon. This involves a wide range of considerations not only from a legal perspective but also in terms of tax and accounting. Given that cross-border corporate restructurings are not actions that can easily be reversed, it is important to consult with professional advisors, including law firms, at an early stage, even when a listing is only being considered.

Goto

By way of further detail on JDRs, a framework broadly equivalent to domestic listed shares is in place, including timely disclosure in Japanese, information dissemination through TDnet, and dividend payments in Japanese yen. The flexibility to achieve a TSE listing without significantly altering the existing shareholder structure, place of incorporation, or overseas fundraising arrangements is an important advantage for startups that have received equity investment.

By contrast, in the case of CI, shares are treated as Japanese equities following listing, which is a significant benefit in that they become eligible for investment by Japan focused equity funds.

Sato

Which scheme is more suitable will depend on factors such as the company’s capital structure, management strategy, and business scale. As a general matter, there is no single answer as to which is superior, and the decision must be made on the basis of a careful analysis of each company’s specific circumstances.

That said, one point applies in either case: leaving the choice of listing structure until just before the IPO is likely to be the least efficient approach. Startups and venture capital investors with an interest in this area should begin consulting the relevant professional advisers as early as possible.

Goto

From our perspective, we welcome listings on TSE through either JDRs or CI. We aim to work closely with all relevant stakeholders to support each company in selecting the most appropriate structure based on its specific circumstances.

Future Outlook ──

── We would like to ask you to share your views on the future direction of the TSE Asia Startup Hub.

Goto

In 2025, a company from the Philippines was added to the program, further expanding its geographic reach. While placing emphasis on the “quality” of participating companies, including their business fit with the Japanese market and their projected scale over the longer term, we aim to support a more diverse range of companies across different regions and industries.

The project was launched with the concept of “working alongside companies from four to five years prior to listing,” and some of the companies selected in 2024 have already begun to enter the concrete IPO preparation phase. The emergence of successful cases among these companies is expected to serve as a strong impetus for those that follow.

Accumulating successful examples of Asian startups listing on TSE will not only encourage other overseas companies but also serve as a catalyst for domestic startups and large corporations, ultimately contributing to the revitalization of the Japanese economy as a whole. We intend to continue working together with our partners to generate many such success stories and to further develop this ecosystem.

Sato

From the perspective of a law firm, one point to add is that there are many stages at which continuous legal support is required, including initial business expansion into Japan, business partnerships with Japanese companies, the TSE IPO examination process, and the maintenance of systems and compliance as a listed company following IPO, such as investor relations, governance enhancement, and M&A. In this context, if law firms are able to support overseas clients from an early stage through the TSE Asia Startup Hub, it would enable both sides to develop a deep mutual understanding of the business and cultural differences, help minimise communication gaps, and ultimately build a strong and effective long-term working relationship.

From TMI’s perspective, we value building long-term relationships with companies supported under the TSE Asia Startup Hub, as well as those that may become future candidates, and aim to be trusted partners that can work alongside them both before and after listing.

── Finally, we would like to ask you to share a message for startups across Asia.

Goto

Japan offers one of the world’s leading capital markets, a strong base of high-quality manufacturing and technology companies, and a stable consumer market. For Asian startups, these are valuable assets that should not be overlooked. We encourage you to take the first step into the Japanese market through the TSE Asia Startup Hub.

We welcome approaches from a wide range of stakeholders, including companies seeking to expand into Japan as well as investors who have made equity investments in such businesses.

Sato

We are seeing firsthand a growing momentum in which talented entrepreneurs across Asia are forming deeper connections with the Japanese market and achieving mutual growth, and we hope this trend will continue to strengthen.

From the perspective of a corporate lawyer with experience on secondment to the TSE and having completed an MBA, I am convinced that the TSE Asia Startup Hub is a highly practical and meaningful initiative, and one that will contribute positively to the Japanese economy.

As one of the partners of the TSE Asia Startup Hub, TMI is committed to contributing to the efforts. If you are interested, even at an initial stage of simply learning more, we would be pleased to hear from you. Please feel free to reach out to our team in Singapore, as well as TMI members in Japan and other countries. Thank you very much for your time today.

Member

PROFILE

SHARE![]()

![]()

![]()